Understanding how bank De-risking works, how it impacts us and what Bitt will change.

Understanding how bank De-risking works, how it impacts us and what Bitt will change.

Wednesday night you are enjoying a quiet dinner with your significant other after a long day of work, some much needed down time. Your phone pings, probably another work related email. After some deliberation you decide to give it a quick scan incase it’s an emergency. The credit card company you set to monthly auto pay emailing to let you know the bank payment was declined. What…? But you have a decent stash in that savings account. Not understanding what has happened, you decide to leave it until tomorrow morning, it can wait. You don’t want it to ruin your dinner. When we sit on the right side of the fence we are removed from the harsh realities, until we aren’t. It’s hard to understand the sting of a bee until it bites you.

Here is a real client who was directly impacted by this unsavoury phenomenon:

“I have been a customer of HSBC for more than 30 years. My balance stood at over £100,000. HSBC closed both my UK and expat accounts (I live in Tanzania) so I have no access to my funds and am unable to open another UK account. Customer service just keeps repeating that the banking terms and conditions allow HSBC to close my accounts and that the decision will not be reversed. It feels like being sentenced for an unspecified crime without being able to represent myself or appeal the decision.”

The 2008 financial crisis has left a marred landscape of far reaching consequences, including a shift in the relationship between regulatory authorities and financial institutions. Responding to the accusations that financial institutions were remiss in their duties before the crisis, US regulators have increased scrutiny on financial services. This has manifested itself in increased focus on AML/CFT requirements.

Financial institutions have responded by drastically scaling back their risk, which has germinated in the wholesale closure of entire customer bases. Financial institutions use different procedures and benchmarks to assess the termination of a customer account. They do not publicly release the criteria they use in determining when a customer will be formally exiled.

These standards vary greatly across financial institutions mainly due to a few factors:

- Appetite for risk

- Risk absorption capacity

- Bank size

- Potential profit modelling and forecasts

- Regulatory climate

- Cost of effective compliance AML/KYC policies

- Respective fines and penalties

- Reputational and legal concerns

- Shift from corporate responsibility to individual liability

Regrettably, businesses rarely consider the impacts their actions/decisions have on their respective clients. Here in the Caribbean we don’t have many choices, people have become quite comfortable with the payment methods they currently use. This began and ended with pin numbers and credit/debit cards, little to no innovation has happened in this sector.

The security and efficiency of credit cards are abysmal; standing there in front a sea of people and cameras while you input your “secret pin,” or physically pulling out a card containing your “private key;” – The same set of numbers which change every 3-5 years, regardless of how many times you use it. But we won’t dive deeper into the nuances which make credit/debit so vulnerable and inefficient, or it will hijack this post – Those two points should be enough to get the newer users scratching their chin.

If we the consumers take a step back

and observe the financial services sector, we will notice they are

pivoting quite aggressively. Investing, researching, creating and buying

anything with the word “Blockchain” – The world is slowly realizing

that Bitcoin has a more elegant solution to the problem which financial

services have long considered unsolvable (and incidentally, quite

profitable).

Financial institutions are in an

‘investigative phase’ with regard to blockchain technology; taking the

parts of the technology that suits their needs, and using it to improve

their own systems. However, blockchain technology, like other

groundbreaking technological advances before it, has the ability to

scale or ‘snowball’ in a way these financial institutions may not be

prepared for.

What does this mean for consumers though? For the people who wants to purchase some groceries, buy that pizza, or purchase that lit game which is on 60% discount through steam sales (#ThanksGaben) – it means we can start to break down financial barriers between markets and people around the world; we can start experimenting with the peer-to-peer connectivity we are familiar with in other sectors. It means we finally connect with each other in a way we’ve long been precluded from by the existing financial system.

Suppose you were one of the many unfortunate cases which the bank/financial service isolated and shut down, you thankfully managed to get your money out, now what? Planning to live like Pablo Escobar? Bury our cash like squirrels? Buy a safe and live in perpetual anxiety?

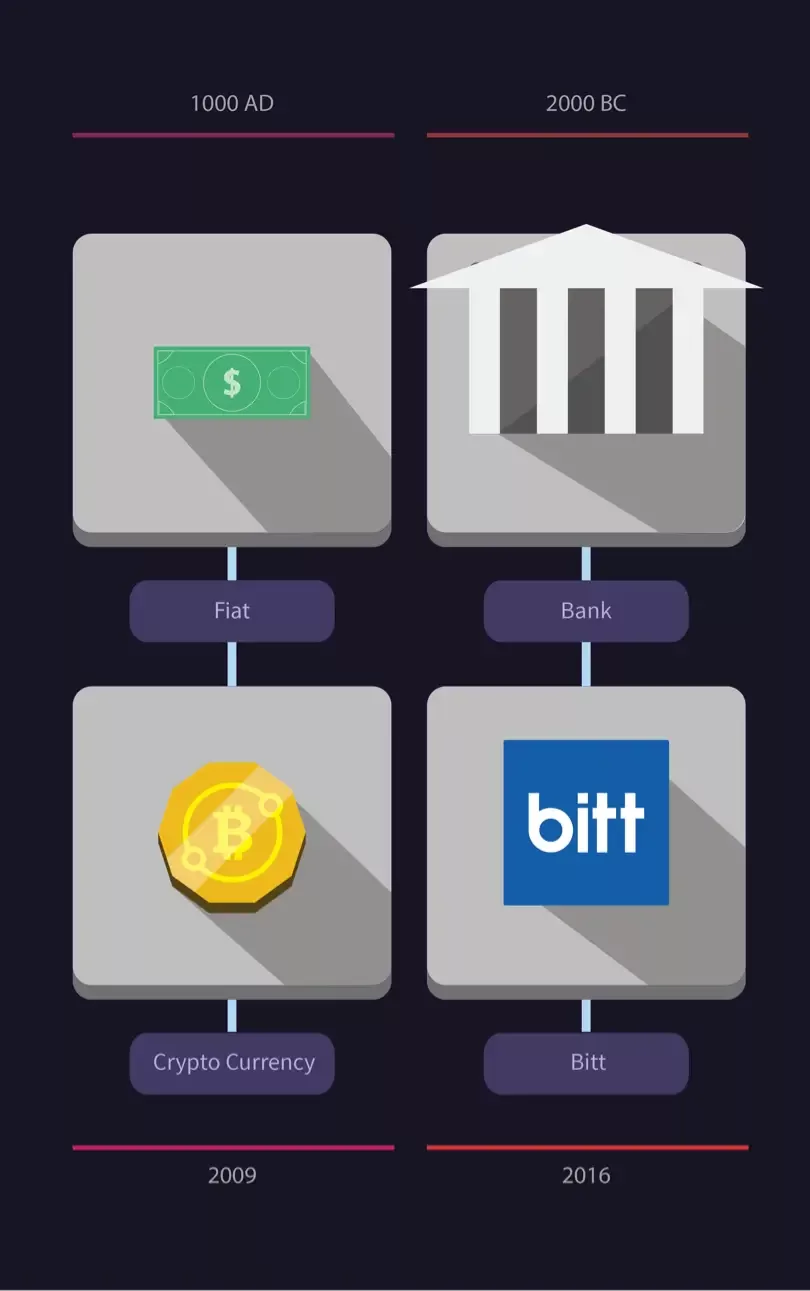

Digital currency is reshaping the financial services landscape, innovation in this space has been long overdue. Somewhere we can safely store our money, where we can operate with total financial inclusion without fear of someone ‘freezing’ our funds. The ability to send value seamlessly and securely utilising THE Blockchain – as in the bitcoin blockchain – and not some privately owned centralized wannabe.

Bitcoin technology – The protocol and the cryptography – has a robust security track record. The network is probably the biggest distributed computing project in the world. The code is open source with nothing to hide; continuously attacked and pushed by hackers and companies throughout the world since the early days.

The 10+ Billion dollar bounty on the network makes for quite the bullseye, this isn’t some flimsy bootstrapped version of Paypal. It is an elegant and honest solution to a host of issues across multiple sectors, and the untapped potential of this technology is enormous. The lid of Pandora’s box is removed and it there is no undo button.

Bitt has extended it’s hand and offers a myriad of financial services, with a dedicated and brilliant team committed to innovating on the bitcoin blockchain. Bitt is going to make this as easy as possible. Load up on your digital dollars, get your Bitt credit card or download the mobile app. Go to that store and swipe, scan, and buy. Financial inclusion has arrived for those who want change or had no other options, we finally have some truly innovative digital solutions – welcome to the digital age.

Read More Related Content: